How Long Will My Savings Last? Exploring Smart Retirement Investment Options

Table of contents

- Why passive income matters for early retirement

- Planning for retirement at 55

- Traditional retirement accounts and their limits

- The case for retirement income diversification

- 5 passive income streams to consider

- Getting professional guidance

- Building a smarter retirement income plan

- Frequently asked questions

Most retirees will need

80%*

of their pre-retirement income to maintain their lifestyle but traditional investments alone may not reliably generate that level of income.

Retiring early or planning for financial flexibility requires more than simply saving — it requires strategically building multiple streams of income. While 401(k)s, Individual Retirement Accounts (IRAs), and Social Security provide a foundation, relying solely on these accounts may leave gaps in your retirement cash flow, especially if you want to preserve capital and avoid drawing down investments too quickly.

For many investors, the key lies in passive income strategies — investments that aim to generate cash flow without daily management. These can range from dividend-paying stocks to real estate investments professionally managed by others. Starting early allows your portfolio to grow over time, potentially providing substantial income well before retirement.

In this guide, we’ll explore five passive income strategies for early-retirement-minded investors, including a little-known option: investing in real estate without becoming a landlord.

Why Passive Income Matters If You Want to Retire Early

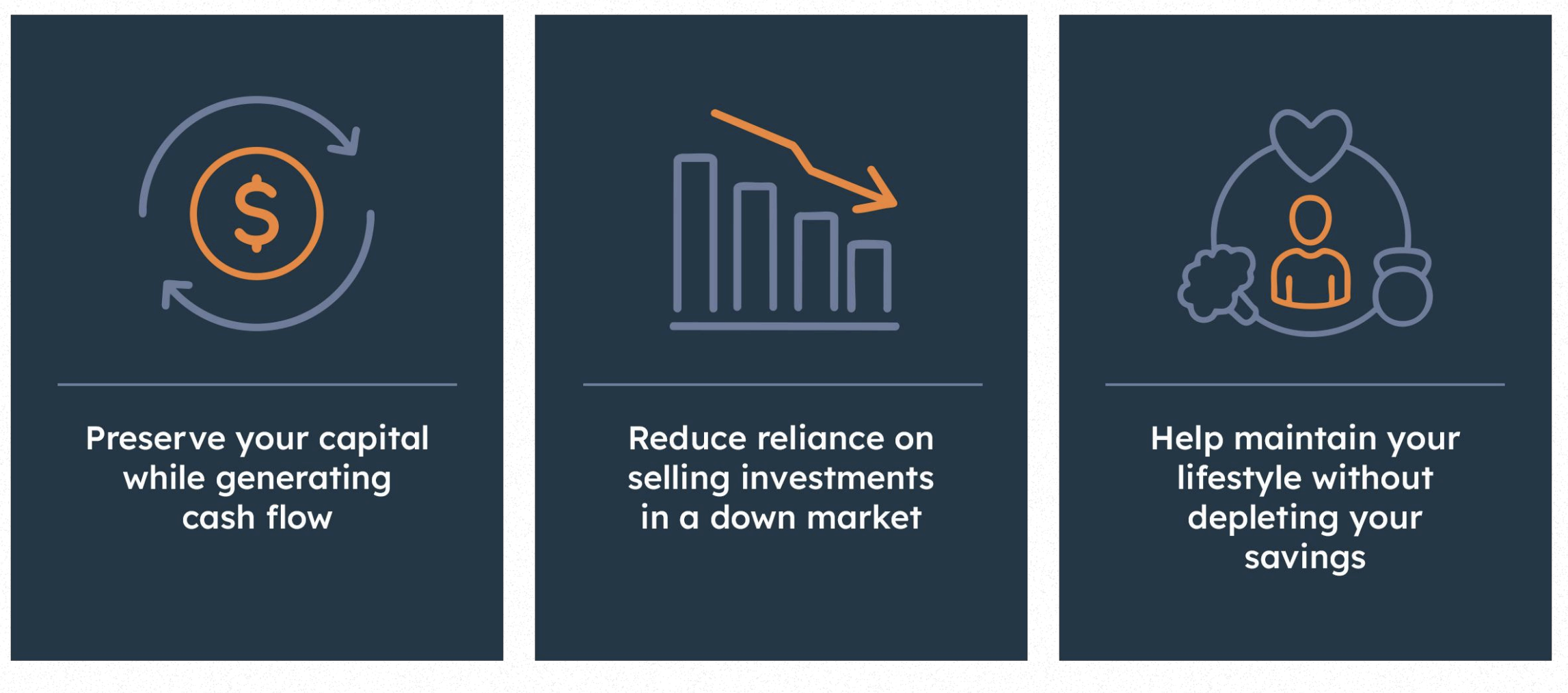

Planning for retirement at 55 or even 60 requires a strategy beyond traditional accounts. Passive income could possibly:

Relying solely on Social Security or a single retirement account exposes investors to sequence-of-returns risk — the danger of withdrawing money during market downturns and reducing your portfolio’s longevity. Passive income sources can possibly act as a buffer, helping your portfolio last longer and giving you more confidence to retire on your own terms.

Planning for an Early Retirement Age at 55

Retiring early means your portfolio may need to last 30+ years. Even with a high savings rate, relying only on a 401(k) or IRA may force early withdrawals that compromise long-term growth. Diversified passive income helps bridge this gap, giving your portfolio time to grow while still providing a steady cash flow.

For example, if an investor retires at 55 with $1 million in a 401(k) and plans to withdraw $50,000 per year, any market downturns early in retirement could dramatically reduce the portfolio s longevity. Adding passive income streams such as dividend stocks, fixed income, and real estate can reduce the need for early withdrawals, providing a means to protect your capital.

Covering Income Gaps Without Relying Only on a 401(k) or IRA

While tax-advantaged retirement accounts are essential, they often come with contribution limits, withdrawal restrictions, and potential penalties for early withdrawals. For 2026, the 401(k) contribution limit is $24,500. Roth IRAs are capped at $7,500 per year for those under the age of 50, and $8,600 if you’re 50 or older. Complementing these accounts with other income-generating assets — like dividend-paying stocks, real estate, or private funds — can help give you flexibility, stability, and peace of mind. By combining traditional retirement accounts with alternative strategies, investors can work towards creating a robust, multi-layered income plan.

Traditional Retirement Accounts and Their Limits

401(k)s, Roth IRAs, and traditional IRAs are powerful tools, but they aren’t always enough for early retirees. Understanding their limitations is key to building a sustainable income plan.

Using a Roth or 401(k) Retirement Calculator to Stress-Test Your Plan

A retirement calculator can help model* how long your savings might last, factoring in:

- Expected returns for different asset classes

- Inflation and cost-of-living adjustments

- Withdrawal strategies and timing

*Results may not reflect the impact of economic and market fluctuations

Stress-testing your retirement plan allows you to identify potential gaps and explore how passive income sources could supplement your withdrawals, help provide a safety net and potentially extend your portfolio’s lifespan.

Tax-Advantaged Retirement Investing with Stocks, Bonds, and Dividends

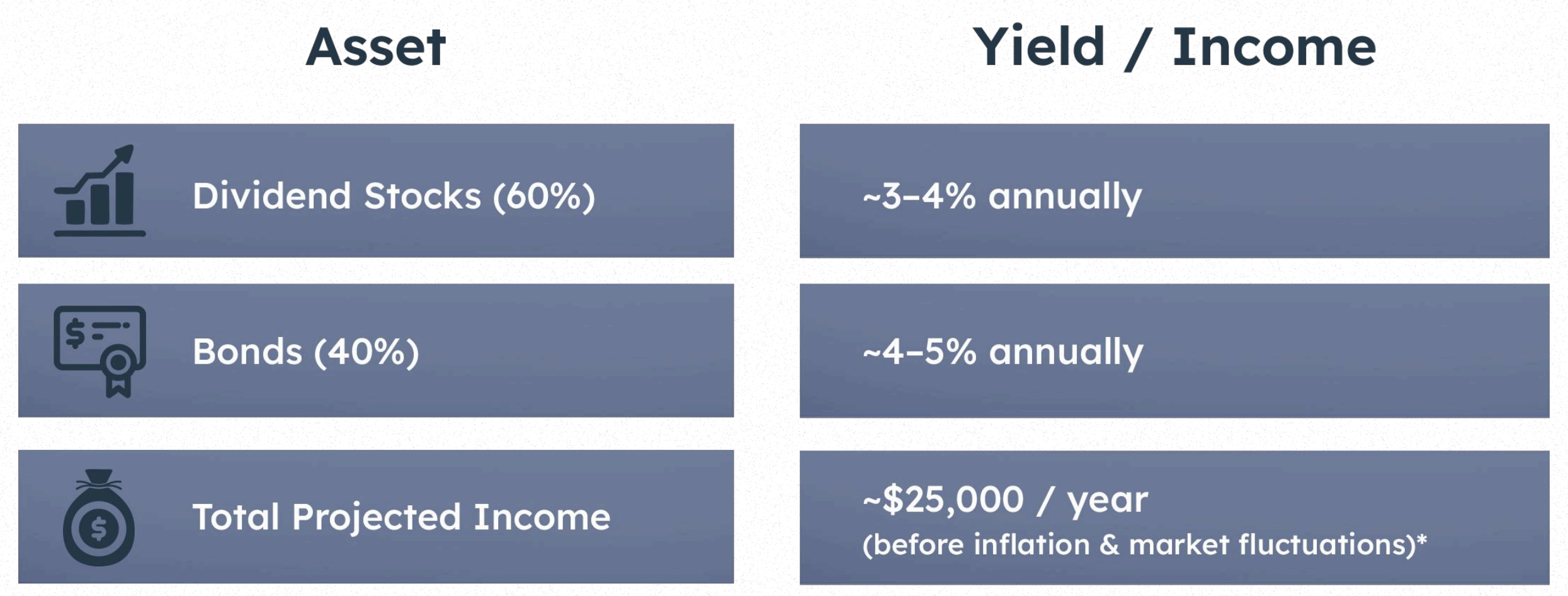

Traditional accounts allow for tax-deferred growth, and Roth accounts offer tax-free withdrawals. Holding dividend stocks, bonds, and other interest-bearing investments in these accounts can possibly maximize income while minimizing taxes — but these accounts alone may not generate sufficient cash flow for long-term early retirement.

For example, consider an investor with a $500,000 Roth IRA invested 60% in dividend-paying stocks and 40% in bonds:

*The projections, estimates, and any modeling tools referenced in this article are provided for illustrative purposes only and are not intended to reflect actual or future performance. These examples are based on assumptions that may not materialize and do not account for all possible variables or real-world conditions.

Actual results may differ materially due to a variety of factors, including but not limited to economic and market fluctuations, changes in interest rates, and other unforeseen events. Modeling tools have inherent limitations and cannot fully predict future outcomes.

This information is intended for general educational purposes only and should not be relied upon as a guarantee of future results or as investment advice. Investors should conduct their own analysis and consult with qualified professionals before making any investment decisions.

While helpful, this may not cover all expenses for an early retiree, highlighting the importance of additional income streams.

The Hidden Constraints of Traditional Accounts for Early Retirees

Early retirees must consider:

- Penalties: Withdrawals from traditional IRAs before age 59½ may incur a 10% penalty.

- Required minimum distributions (RMDs): After age 73, traditional IRAs and 401(k)s require withdrawals, which may affect taxes and income planning.

- Contribution limits: Even maxing out accounts may not generate enough income for an early retirement lifestyle.

Diversifying outside retirement accounts with income-generating investments could help give flexibility, tax efficiency, and long-term stability.

The Case for Retirement Income Diversification

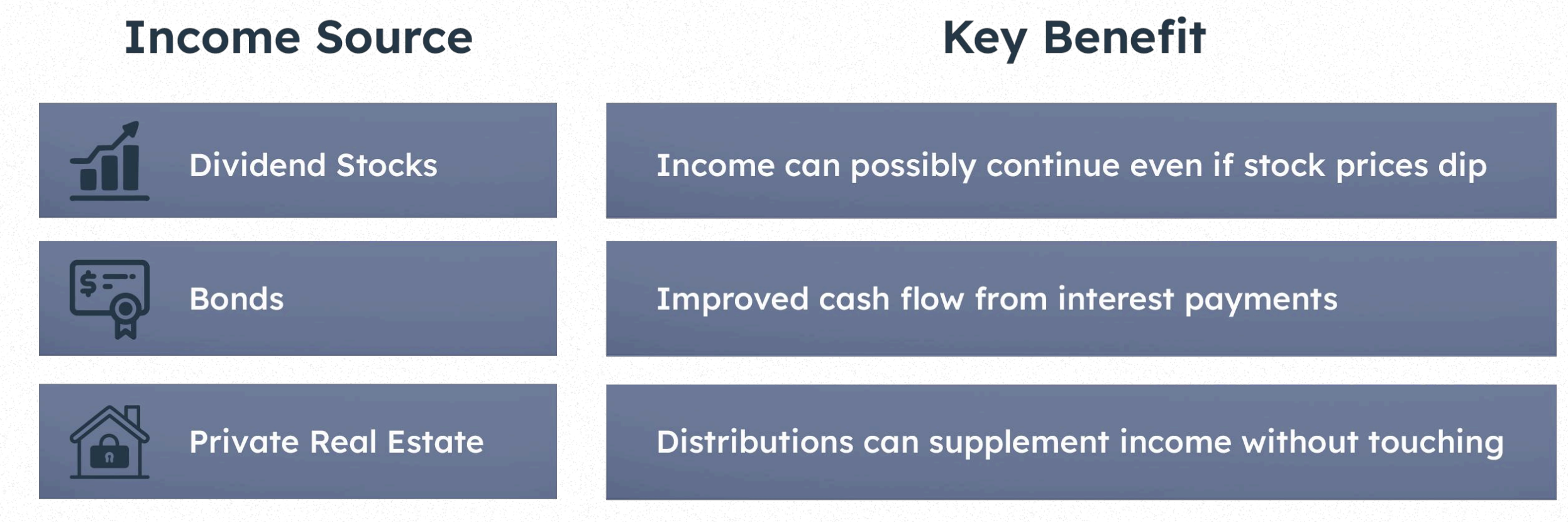

Relying on a single income source is risky. Market volatility, unexpected expenses, or changes in interest rates can disrupt your cash flow. Diversifying across multiple streams including stocks, bonds, cash equivalents, rental income, and private real estate funds can help create a more resilient retirement portfolio.

Why You Shouldn’t Rely Only on Your 401(k) and IRA

Even a well-funded 401(k) may fall short if your retirement starts earlier than expected. Diversifying income streams seeks to reduce dependency on any single source and improves financial security.

How Multiple Income Streams Could Extend the Life of Your Savings

By combining different investments, you can manage risk and possibly reduce the need to sell assets during market downturns. For example:

This approach aims to help your capital grow while providing a reliable cash flow opportunity to fund living expenses.

How Passive Income Helps Potentially Mitigate Portfolio Risk

Passive income acts as a potential buffer against market fluctuations. Even when equities underperform, a possible source of consistent cash flow from other sources helps maintain your lifestyle. A diversified approach aims to reduce sequence-of-returns risk and support a sustainable withdrawal strategy.

5 Passive Income Streams to Consider

1. Dividend Stocks

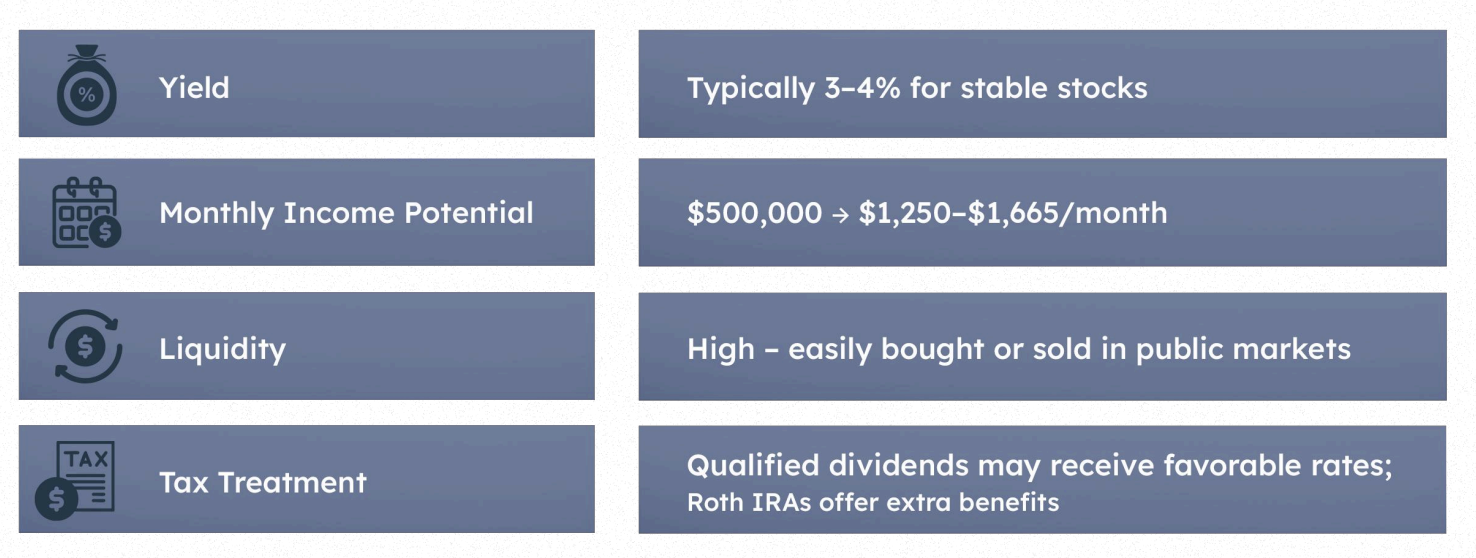

Dividend-paying stocks and ETFs are a cornerstone of many US investors’ passive income strategies. Companies in sectors like utilities, consumer staples, and healthcare often provide steady dividends, offering reliable cash flow while aiming to allow capital to grow

The figures and examples shown above are for illustrative purposes only and are based on a hypothetical scenario. They are intended to demonstrate general concepts and do not represent actual investment results or returns.

Estimated yields, income potential, and tax treatment are subject to change and may vary based on market conditions, individual investment choices, and personal circumstances. Actual dividend income may fluctuate and is not guaranteed.

This example does not account for factors such as market volatility, changes in interest rates, company performance, taxes, fees, or other variables that may impact outcomes. Investors should not rely on this information as a guarantee of future performance and are encouraged to consult with qualified financial and tax professionals before making investment decisions.

Dividend income can fluctuate in volatile markets. Diversifying across sectors and holding stocks in tax-advantaged accounts could potentially optimize after-tax returns.

Additional Insights

Dividend ETFs allow you to invest in dozens or hundreds of companies at once, reducing single-stock risk. Examples include Vanguard Dividend Appreciation ETF (VIG) and Schwab U.S. Dividend Equity ETF (SCHD), which focus on companies with a history of increasing dividends.

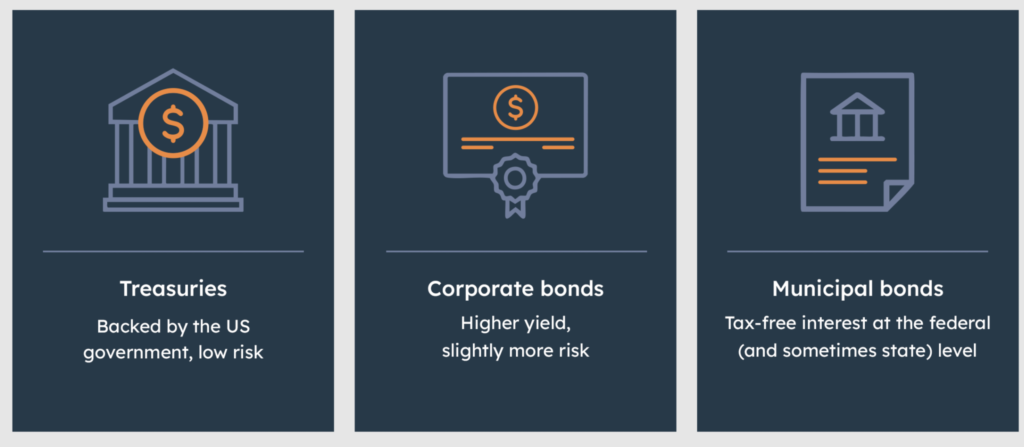

2. Fixed-Income Investments

Bonds, Certificates of Deposit, and other fixed-income vehicles offer steady interest payments and are generally less volatile than equities.

Fixed-Income Investments for Early Retirement

While fixed-income products tend to be lower risk, their returns may struggle to outpace inflation. They historically work best as part of a diversified income stack that aims to balance growth and stability.

Practical Examples

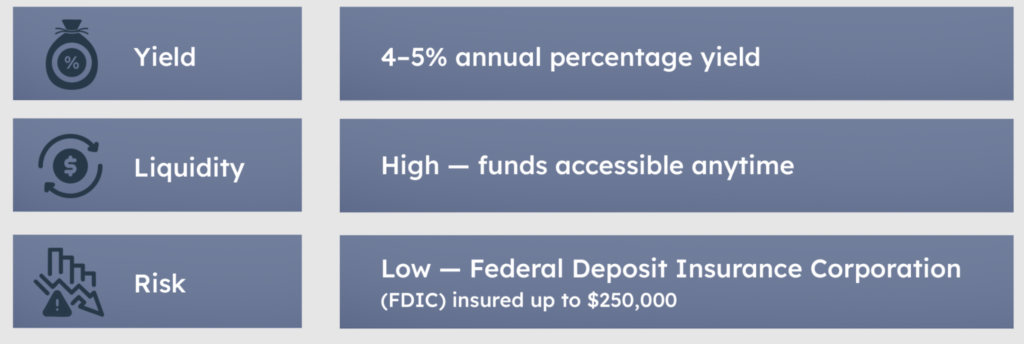

3. High-Yield Savings Accounts (HYSA)

High-Yield Savings Accounts (HYSA) provide liquidity and security, making them ideal for emergency funds or short-term savings.

The figures and examples shown above are for illustrative purposes only and are based on a hypothetical scenario. They are intended to demonstrate general concepts and do not represent actual investment results or returns. Estimated yields, income potential, and tax treatment are subject to change and may vary based on market conditions, individual investment choices, and personal circumstances. Actual dividend income may fluctuate and is not guaranteed. This example does not account for factors such as market volatility, changes in interest rates, company performance, taxes, fees, or other variables that may impact outcomes. Investors should not rely on this information as a guarantee of future performance and are encouraged to consult with qualified financial and tax professionals before making investment decisions.

HYSAs aim to protect capital and provide accessible income, but inflation can erode real returns over time. They are most effective as a relatively safe place to hold cash within your overall portfolio.

4. Expanding Beyond Traditional Markets

For qualified investors, access doesn’t stop at stocks, bonds, and mutual funds. Private market opportunities including private equity, private credit, infrastructure, and institutional-quality strategies open the door to a broader investment universe. These investments are typically structured around multi-year business plans and operational value creation rather than short-term market movements

Why Alternatives Matter

Public markets offer liquidity — but they also bring daily volatility and high correlation during market stress. Private investments can:

- Provide differentiated return streams

- Reduce reliance on public market performance

- Focus on long-term value creation

- Potentially enhance overall portfolio diversification

A Long-Term Mindset

When thoughtfully allocated, they can complement traditional portfolios and support long-term wealth-building strategies.

5. Investing in Property Without Becoming a Landlord

Surveys consistently show that many Americans believe real estate is one of the strongest long-term asset classes — yet relatively few invest beyond their primary residence.

Often, the hesitation isn’t about belief in real estate. It’s about complexity.

Direct rental ownership can offer income and appreciation, but it also involves tenant management, maintenance costs, financing logistics, and ongoing oversight. For busy professionals, business owners, or early retirees, that hands-on commitment may not align with their lifestyle.

A More Passive Approach to Real Estate

Private real estate funds and private REIT structures can offer exposure to professionally managed, income-producing properties including multifamily, commercial, industrial, or mixed-use assets without day-to-day operational responsibilities.

Instead of managing tenants or repairs, investors potentially stand to gain:

- Access to diversified portfolios of institutional-quality assets

- Professional property and asset management

- Income potential aligned with long-term holding strategies

- Structured liquidity designed for patient capital

Private real estate is often considered tax-efficient, and in some cases, distributions may include Return of Capital components that can defer taxes.

For investors who believe in the long-term strength of real estate but prefer a hands-off approach, this structure aims to bridge the gap between conviction and practicality — offering income and growth potential without the responsibilities of being a landlord.

Getting Professional Guidance

A financial advisor can help you see how private real estate funds fit into your overall financial picture. With proper guidance, you can:

- Evaluate whether private funds and other alternative investments are suitable for your goals

- Integrate these investments into your broader retirement and wealth strategy

- Plan for tax considerations and distribution timing to align with your long-term objectives

This ensures your investment choices support your complete financial plan, rather than standing alone.

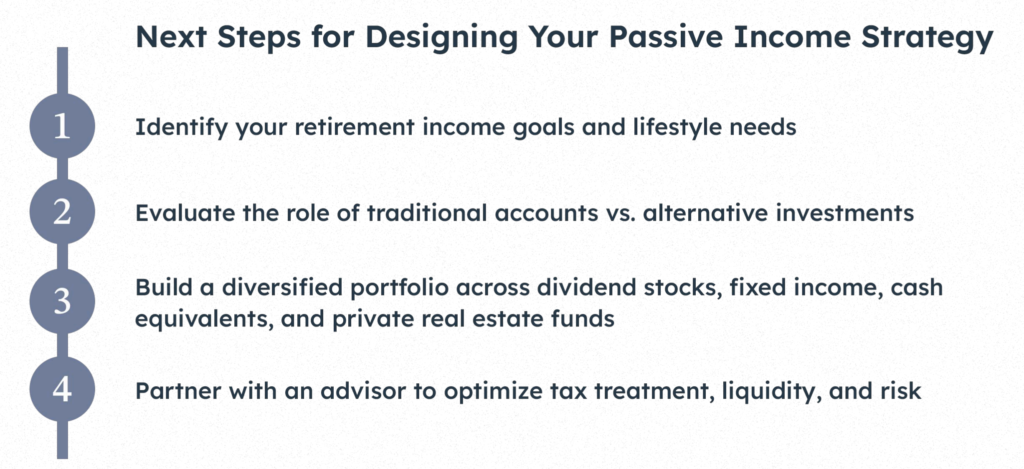

Putting It All Together: Building a Smarter Retirement Income Plan

We believe the most effective retirement income strategies combine multiple sources of cash flow. By balancing growth potential, income stability, and risk, you can create a plan that supports your lifestyle throughout early or flexible retirement.

How Private Real Estate Funds Can Complement Traditional Accounts

- Add real estate exposure without operational responsibilities

- Provide potentially higher distributions than traditional stocks or bonds

- Integrate with 401(k)s, Roth IRAs, and taxable accounts for tax efficiency

FAQ / Related Questions

The longevity of your savings depends on factors like your withdrawal strategy, investment returns, inflation, and overall portfolio mix. Retirement planning tools can help you model different scenarios and better understand how your assets may perform over time. Reviewing your plan regularly allows you to make thoughtful adjustments as your goals or circumstances evolve. Adding diversified income sources can help create greater confidence in your long-term outlook.

Passive income can complement traditional retirement accounts by providing an additional layer of cash flow. This can help support your lifestyle while allowing long-term investments more time to grow. A well-balanced mix of income-generating assets may help smooth out fluctuations over time. The goal is to create a structure where different parts of your portfolio work together.

Private real estate funds can provide exposure to professionally managed properties without the day-to-day responsibilities of ownership. They are typically structured with a long-term mindset, aligning with many retirement planning horizons. When thoughtfully incorporated alongside traditional accounts and public market investments, they can broaden diversification. As with any investment decision, it’s important to ensure it aligns with your overall financial picture.

A strong retirement plan often includes both. Growth-oriented investments help your portfolio keep pace with inflation over time, while income-focused assets provide cash flow to support your lifestyle. Finding the right balance depends on your timeline, goals, and comfort level. A diversified approach can help create stability while supporting long-term financial sustainability.

No matter when you envision retiring, starting early and planning carefully can make a meaningful difference. Multiple streams of passive income give you flexibility, security, and the freedom to retire on your terms.

Take the Next Step Toward Retirement Confidence

- Sign up for expert insights on passive income strategies

- Learn how private real estate funds can fit into your retirement plan

- Follow us on social media to stay up to date with the latest news and trends

Disclaimers: Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Equiton Capital LLC. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Equiton Capital LLC or any other person. While such sources are believed to be reliable, Equiton Capital LLC does not assume any responsibility for the accuracy or completeness of such information. Equiton Capital LLC does not undertake any obligation to update the information contained herein as of any future date.

Not an Offer, Recommendation or Professional Advice: This writing does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the reader has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact Equiton Capital LLC or consult with the professional advisor of their choosing.

Past Performance: There is no guarantee that the investment objectives will be achieved. Moreover, the past performance is not a guarantee or indicator of future results.

Forward-Looking Statements: Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

The information provided in this article is for general educational purposes only and does not constitute investment, legal, or tax advice, nor should it be relied upon as a recommendation or an offer to buy or sell any security.

Investing in real estate and real estate investment trusts (REITs) involves risks, including but not limited to fluctuations in property values, changes in interest rates, tenant vacancies, refinancing risk, and broader economic or market conditions. REITs may also be subject to liquidity constraints, leverage-related risks, and sector or geographic concentration risks, all of which can impact income and the value of an investment.

Diversification is often used as a risk management strategy; however, it does not ensure a profit and does not protect against loss in declining markets. All investments carry risk, and past performance is not indicative of future results.

Investors should carefully consider their financial objectives, risk tolerance, and investment time horizon and should consult with qualified financial and tax professionals before making any investment decisions.

Stay Connected

Sign up to receive more real estate insights straight to your inbox and explore strategies, market trends, and educational resources designed for accredited investors seeking passive income through real estate.